Medicare Part C in medical billing, commonly called Medicare Advantage, covers nearly half of all Medicare beneficiaries in the United States. For healthcare providers, that means a large share of your Medicare patient population is not actually billed through Original Medicare.

They are billed through private insurance companies that operate under Medicare rules but apply their own plans, networks, and policies on top of them.

If your billing team is treating Medicare Advantage claims the same way it treats traditional Medicare, that is a problem. The billing workflows, network rules, authorization requirements, and reimbursement processes differ in ways that directly affect your revenue.

This guide covers what Medicare Part C is, how it affects billing at your practice, and what your team needs to handle it correctly.

What is Medicare Part C in Medical Billing?

Medicare Part C is the part of the Medicare program that allows private insurers to offer Medicare coverage.

Rather than receiving benefits directly from the federal government through Original Medicare, a beneficiary enrolled in Part C gets their coverage through a private plan that has been approved by the Centers for Medicare and Medicaid Services.

These plans must cover everything that Original Medicare Parts A and B cover. Many also include prescription drug coverage (Part D), along with extra benefits like dental, vision, and hearing coverage that Original Medicare does not provide.

From a billing standpoint, the key fact is this: when you treat a Medicare Advantage patient, you are not billing Medicare. You are billing the private insurance company that administers that specific plan.

Medicare Part C vs. Original Medicare: The Billing Difference

Original Medicare (Parts A & B) is the government’s basic health plan. It lets you see doctors anywhere in the U.S. who accept Medicare. You usually pay 20% of costs after any deductible, with no yearly limit on out-of-pocket spending.

Medicare Advantage (Part C) is run by private companies. It covers everything in Parts A and B, and often prescription drugs. It usually has lower premiums, extra perks like dental and vision, but you must use their providers’ network. But it caps your yearly out-of-pocket costs.

Who You Are Billing

With Original Medicare, claims go to the Medicare Administrative Contractor (MAC) for your region. With Medicare Advantage, claims go directly to the private insurer, such as UnitedHealthcare, Humana, Aetna, or Blue Cross. Each insurer has its own billing requirements, prior authorization rules, and claims portals.

Fee Schedules

Original Medicare uses a national fee schedule published by CMS. Medicare Advantage plans negotiate their own reimbursement rates with providers. These rates can be higher or lower than the standard Medicare fee schedule depending on the plan and the contract you have signed.

Prior Authorization

Original Medicare does not require prior authorization for most services. Medicare Advantage plans can and do require prior authorization for a wide range of services, including specialist visits, imaging, surgery, and inpatient admissions. Missing a required authorization is one of the top denial reasons for Medicare Advantage claims.

Network Rules

Original Medicare works with any provider who accepts Medicare assignment, regardless of geography. Medicare Advantage plans often restrict coverage to specific provider networks. Some plans are HMOs that require in-network care except in emergencies. Others are PPOs that allow out-of-network care but at higher cost-sharing for the patient.

| Billing Medicare Advantage correctly across multiple plans takes specific expertise. Book a free consultation with SwiftCare Billing to find out if your practice is leaving money on the table. Call (848) 359-5702 or visit swiftcarebilling.com. |

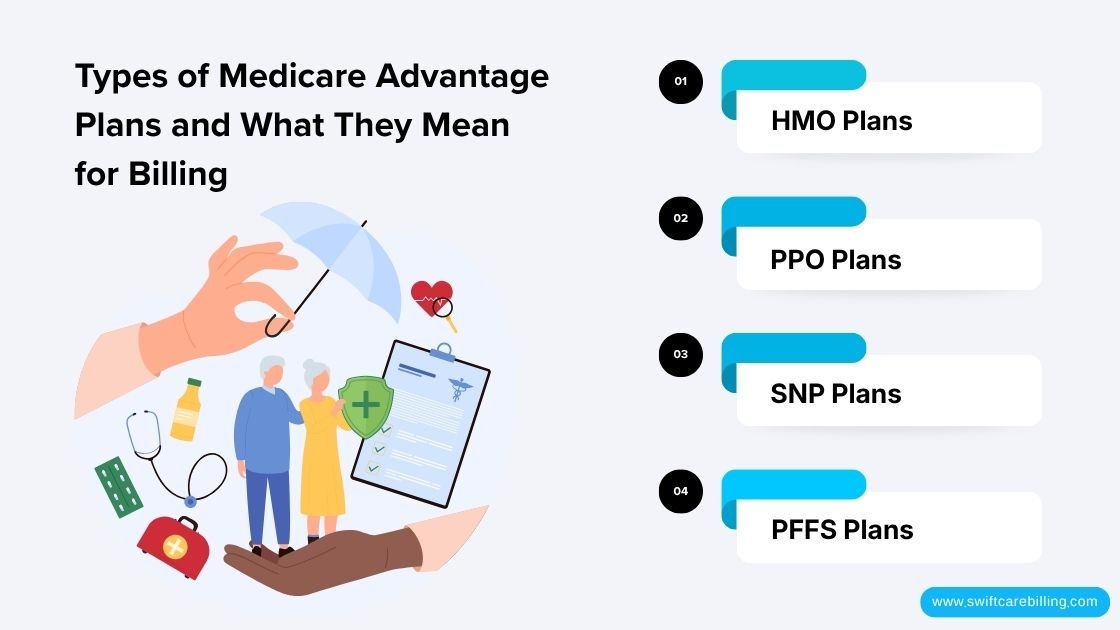

Types of Medicare Advantage Plans and What They Mean for Billing

1. HMO Plans

Health Maintenance Organization plans require patients to use in-network providers and typically require a referral from a primary care physician before seeing a specialist. For your billing team, this means verifying network status and referral requirements before every visit.

2. PPO Plans

Preferred Provider Organization plans allow patients to see providers outside the network, but at higher out-of-pocket costs. Billing an out-of-network patient under a PPO requires knowing the plan’s out-of-network reimbursement rate and communicating the patient’s higher cost-sharing responsibility upfront.

3. SNP Plans

Special Needs Plans serve specific populations, including patients with chronic conditions (Chronic Condition SNPs), dual eligibles who have both Medicare and Medicaid (Dual SNPs), and patients in institutional care (Institutional SNPs). Billing these plans often involves coordination with Medicaid for patients who are dual eligible.

4. PFFS Plans

Private Fee-for-Service plans set their own payment terms. Providers who see PFFS patients must agree to the plan’s terms for each encounter. Some PFFS plans are network-based; others allow any provider to agree to treat the beneficiary under the plan’s terms.

Key Medical Billing Requirements for Medicare Advantage

Let us talk about some important requirements for Medicare billing.

Credentialing and Network Participation

Before you can bill a Medicare Advantage plan, you must be credentialed and accepted into that plan’s network. Credentialing is a separate process from Medicare enrollment. Each Medicare Advantage plan operates its own credentialing process, and the timelines can run from 60 to 120 days.

If your practice is still working through credentialing, see our credentialing services for support with Medicare Advantage and other commercial payers.

Prior Authorization Management

Tracking prior authorizations across multiple Medicare Advantage plans requires a reliable system. Each plan has different requirements, different portals, and different turnaround times. A single missed authorization can mean a full denial on a high-dollar claim.

- Confirm authorization requirements at the time of scheduling

- Obtain the authorization number and include it on the claim

- Track expiration dates, particularly for recurring or ongoing services

- Document authorization attempts in case of denial appeals

Timely Filing Limits

Medicare Advantage plans set their own timely filing windows, which can range from 90 days to one year. These windows are separate from the timely filing rules under Original Medicare. Submitting outside the window results in a denial that generally cannot be appealed.

Coordination of Benefits

For dual eligible patients who have both Medicare Advantage and Medicaid, claims may need to be submitted to both payers. The order of payment and how the two plans coordinate benefits depend on the specific plan type and the state’s Medicaid rules.

What Providers Get Wrong with Medicare Advantage Billing

Assuming It Bills Like Original Medicare

A claim that would sail through under traditional Medicare can deny under a Medicare Advantage plan because of a missing authorization, an out-of-network issue, or a plan-specific coverage restriction. The code set is the same; the rules around it are not.

Overlooking the Explanation of Benefits

Medicare Advantage plans issue Explanation of Benefits documents when claims are processed. These explain how the claim was adjudicated, what was paid, and what adjustments were applied. Not reading the EOB carefully leads to payment posting errors and missed appeal opportunities.

Missing Appeals Windows

Medicare Advantage plans must follow federal requirements for appeals, which are more structured than commercial payer processes. Providers have the right to appeal denied claims, and there are defined timelines for each level of appeal. Missing those windows costs you the ability to recover the payment.

| Do not let Medicare Advantage billing complexity cost your practice revenue. SwiftCare Billing handles prior authorizations, claims submission, and denial management across all Medicare Advantage plans. Book your free consultation now. |

How Medicare Advantage Affects Revenue Cycle Management

Impact on Accounts Receivable

Medicare Advantage claims that deny or require additional documentation add days to your accounts receivable. Practices with a high Medicare Advantage census and a weak authorization and follow-up process often see their AR stretch beyond 60 days for this patient population.

Impact on Reimbursement Rates

Your reimbursement rate under a Medicare Advantage plan depends entirely on the contract you have negotiated with that insurer. Rates vary significantly between plans and between specialties. Reviewing your contracts against your actual reimbursement amounts is a step many practices skip but should not.

Impact on Patient Collections

Medicare Advantage plans often have lower premiums than Medicare Supplement plans, but higher out-of-pocket costs at the point of service. Patients may be surprised by their cost-sharing responsibility. Transparent communication about patient balances before the visit reduces disputes and improves collection rates.

Medicare Advantage Audits and Compliance

CMS has increased audit activity around Medicare Advantage plans, particularly around risk adjustment and accurate condition reporting. The CMS Medicare Advantage program page provides current program information for providers.

For providers, the compliance risk is primarily around accurate documentation and coding. Conditions coded in risk adjustment must be actively addressed and documented in the medical record. Unsupported codes identified in an audit can result in payment recoupment.

- Document all chronic conditions that are monitored, treated, or managed

- Do not code conditions from prior years without verifying they are still active

- Ensure medical records support every condition code on the claim

Frequently Asked Questions About Medicare Part C in Medical Billing

Do I need separate credentialing for Medicare Advantage?

Yes. Enrollment in Original Medicare does not automatically grant you participation in any Medicare Advantage plan’s network. Each plan requires its own credentialing application and approval.

Can a patient see me if I am not in their Medicare Advantage network?

It depends on the plan type. HMO plans generally require in-network care except for emergencies. PPO plans allow out-of-network care, but the patient pays more. PFFS plans allow any provider who agrees to the plan’s terms.

Before seeing a Medicare Advantage patient as an out-of-network provider, confirm both the plan’s rules and the patient’s financial responsibility.

How do I know which Medicare Advantage plan a patient has?

The patient’s insurance card will identify the plan name and the insurance company administering it. Eligibility verification before the visit should confirm plan details, coverage, and whether you are in-network for that specific plan.

What happens if I submit a Medicare Advantage claim to regular Medicare?

The claim will likely be rejected. Medicare Advantage patients should not be billed through the Original Medicare system. The claim must go to the private insurer administering the patient’s plan.

Are Medicare Advantage reimbursement rates always lower than Original Medicare?

Not necessarily. Reimbursement rates under Medicare Advantage depend on the contract negotiated between the insurer and your practice. Some plans pay above the Medicare fee schedule; others pay below it. Reviewing your contracts periodically matters.

Get Medicare Advantage Billing Right with SwiftCare Billing

Medicare Advantage is not going away. More of your Medicare patients will be enrolled in private plans every year. Practices that have a strong, plan-aware billing process capture more of what they are owed. Those that treat all Medicare the same leave a predictable amount of revenue behind.

| Book a free consultation with SwiftCare Billing. We handle Medicare Advantage credentialing, prior authorization, claims submission, and denial management so your team can stay focused on patient care. Call (848) 359-5702, email info@swiftcarebilling.com, or visit swiftcarebilling.com. |